Datacamp: https://campus.datacamp.com/courses/quantitative-risk-management-in-python

Course Description

Managing risk using Quantitative Risk Management is a vital task across the banking, insurance, and asset management industries. It’s essential that financial risk analysts, regulators, and actuaries can quantitatively balance rewards against their exposure to risk. This course introduces you to financial portfolio risk management through an examination of the 2007—2008 financial crisis and its effect on investment banks such as Goldman Sachs and J.P. Morgan. You’ll learn how to use Python to calculate and mitigate risk exposure using the Value at Risk and Conditional Value at Risk measures, estimate risk with techniques like Monte Carlo simulation, and use cutting-edge technologies such as neural networks to conduct real time portfolio rebalancing.

1/4 Object:

- understanding of risk and return

- how risk and return are related to each other,

- identify risk factors, and use them to re-acquaint ourselves with Modern Portfolio Theory applied to the global financial crisis of 2007-2008.

Introduction

- Quantitative Risk Management: Study of quantifiable uncertainty

- Uncertainty: (1) Future outcome (2) Outcomes impact planning decisions

- Risk Management: mitigate (reduce effects of) adverse outcomes

- Quantifiable uncertainty: identify fators to measure risk (what factors can cause the uncertainty)

- This project: Focus upon risk associated with a financial portfolio

This project

The Great Recession (2007-2010)

- Global growth loss more than $2 trillion

- United States: nearly $10 trillion lost in household wealth

- U.S. stock markets lost c. $8 trillion in value

Global Finacial Crisis (2007-2009)

- Large-scale changes in fundamental asset values

- Massive uncertainty about future returns

- High asset returns volatility

- Risk management critical to success or failure

Financial portpolios

- Collection of assets with uncertain future returns

- Stocks

- Bonds

- Foreign exchange holdings (‘forex’)

- Stock options

Challenge: Quantify risk to manage uncertainty

- Make optimal investment decisions

- Maximize portfolio return, conditional on risk appetite

Quantifying return

Portfolio return: weighted sum of individual asset returns

pandasdata analysis library- DataFrame

prices .pct_change()method

1 | prices = pandas.read_csv("portfolio.csv") |

Quantifying risk

- Portfolio return volatility = risk

- Calculate volatility(波动率) via covariance matrix(协方差矩阵)

- Use

.cov()DataFrame method ofreturnsand anaualize - Diagonal of

covarianceis individual assets variances - Off-diagonal of

covarianceare covariances between assets

| Assets 1 | Assets 2 | Assets 3 | Assets 4 | |

|---|---|---|---|---|

| Assets 1 | Diagonal | Off-diagonal | Off-diagonal | Off-diagonal |

| Assets 2 | Off-diagonal | Diagonal | Off-diagonal | Off-diagonal |

| Assets 3 | Off-diagonal | Off-diagonal | Diagonal | Off-diagonal |

| Assets 4 | Off-diagonal | Off-diagonal | Off-diagonal | Diagonal |

1 | covariance = returns.cov()*252 |

Portfolio risk

The portfolio variance is a quadratic function of the weights given the covariance matrix, which can be computed in Python using the “At” operator. The variance is usually then transformed into the standard deviation, resulting in the portfolio’s volatility. Both variance and standard deviation are used as measures of volatility.

- Depends upon asset weights in portfolio

- Portfolio variance (方差) = weight矩阵转置 covariance 协方差 weight

- Matrix multiplication can be computed using

@operator in python - Standard deviation (标准差) is usually used instead of variance (方差), 标准差是方差的平方根

1 | weights = [0.25, 0.25, 0.25, 0.25] |

Volotility time series(时间序列)

- Can also calculate portfolio volatility over time

- Use a ‘window’ to comput volatiity over a fixed time period (e.g. a week, 30-day ‘month’)

series.rolling()creates a window- Observe volatility trend and possible extreme events

1 | windowed = portfolio_returns.rolling(30) |

Excercises

quantifying the effects of uncertainty on a financial portfolio

examine the portfolio’s return

1 | # Select portfolio asset prices for the middle of the crisis, 2008-2009 |

1 | # Compute the portfolio's daily returns |

assess the riskiness of the portfolio using the covariance matrix to determine the portfolio’s volatility

1 | # Generate the covariance matrix from portfolio asset's returns |

Q: Which portfolio asset has the highest annualized volatility over the time period 2008 - 2009?

A: Citibank

(the highest along the diagonal of the covariance matrix.)

1 | # Compute and display portfolio volatility for 2008 - 2009 |

1 | # Calculate the 30-day rolling window of portfolio returns |

Risk factors and financial crisis

Risk factors

- Valatility: measure of dispersion(离散程度) of resturns around expected value

- Time series: expected value = sample average

- What drives expectation and dispersion?

- Risk factors: variables or events driving portfolio return and volatility

Risk exposure

Risk exposure: meausre of possible portfolio loss

Risk factors determine risk exposure

Risk Factors

| Type of risk | definition | example |

|---|---|---|

| Systematic risk (系统性风险) | affect volatility of all portfolio assets | e.g. airplane engine failure |

| Market risk | systematic risk from general financial market movements | price level changes, i.e. inflation; interest rate changes; Economic climate changes |

| Idiosyncratic risk (特殊风险,非系统性) | risk specific to a particular asset/asset class | terbulence and the unfastened seatbelt; Bond portfolio: issuer risk of default(违约风险); Firm/sector characteristics: Firm size (market captalization, 市值), Book-to-market(股价净值比) issue, Sector shocks (冲击) |

Factor models

Factor model: assessment of risk factors affecting portfolio return

Satistical regression (统计回归):e.g. Ordinary Least Squares (普通最小二乘法/线性回归)

_ dependent variable (因变量): return (or volatility)

- independent variable (自变量): systemic and/or idosyncratice risk factors

Fama-French factor model: combination of - market risk and

- idiosycratic risk (firm size, firm value)

Crisis risk factor: mortgage-backed securities (MBS 不动产抵押贷款证券)

Investment banks: borrowed heavily just before the crisis (金融危机前大量发债)

Collateral: mortgage-backed securities

MBS: supposed to siversify risk by holdings

- Flaw: mortgage default risk in fact was highly correlated (违约风险高度相关)

- Avalanche of delinquencies (拖延雪崩)/ default destroyed collateral value(抵押价值被破坏)

90-day mortgage delinquency (90天抵押贷款拖欠): risk factor for investment bank portfolio during the crisis

Factor model regression: portfolio returns vs. mortagage delinquency

Import statsmodels.api library for regression tools

Fit regression using .OLS() object and its .fit() method

Display results using regression’s .summary method

1 | import statsmodels.api as sm |

It is the statistical significance of the regression coefficient (回归系数) for mortgage delinquencies that concerns us most.

Exercises

Frequency resampling primer

Risk factor models often rely upon data that is of different frequencies. A typical example is when using quarterly macroeconomic data, such as prices, unemployment rates, etc., with financial data, which is often daily (or even intra-daily). To use both data sources in the same model, higher frequency data needs to be resampled to match the lower frequency data.

The DataFrame and Series Pandas objects have a built-in .resample() method that specifies the lower frequency. This method is chained with a method to create the lower-frequency statistic, such as .mean() for the average of the data within the new frequency period, or .min() for the minimum of the data.

1 | # Convert daily returns data to weekly and quarterly frequency |

结果1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

27

28

29

30

31

32

33

34

35

36

37

38

39

40<bound method NDFrame.head of Date

2004-12-31 NaN

2005-03-31 -0.000367

2005-06-30 -0.000366

2005-09-30 0.000615

2005-12-31 0.001323

2006-03-31 0.001384

2006-06-30 0.000084

2006-09-30 0.001654

2006-12-31 0.001717

2007-03-31 -0.000200

2007-06-30 0.000509

2007-09-30 -0.001446

2007-12-31 -0.002300

2008-03-31 -0.002337

2008-06-30 -0.002166

2008-09-30 0.000943

2008-12-31 -0.003480

2009-03-31 0.002415

2009-06-30 0.004946

2009-09-30 0.004516

2009-12-31 -0.001940

2010-03-31 0.001330

2010-06-30 -0.002688

2010-09-30 0.001088

2010-12-31 0.002328

Freq: Q-DEC, dtype: float64>

<bound method NDFrame.head of Date

2005-01-02 NaN

2005-01-09 -0.011152

2005-01-16 -0.007643

2005-01-23 -0.011076

2005-01-30 -0.000443

...

2010-12-05 -0.009894

2010-12-12 0.001379

2010-12-19 -0.016622

2010-12-26 -0.005974

2011-01-02 -0.007729

Freq: W-SUN, Length: 314, dtype: float64>

Visualizing risk factor correlation

Investment banks heavily invested in mortgage-backed securities (MBS) before and during the financial crisis. This makes MBS a likely risk factor for the investment bank portfolio.

Assess this using scatterplots between portfolio_returns and an MBS risk measure, the 90-day mortgage delinquency rate mort_del.1

2

3

4

5

6

7

8

9

10

11

12# Transform the daily portfolio_returns into quarterly average returns

portfolio_q_average = portfolio_returns.resample('Q').mean().dropna()

# Create a scatterplot between delinquency and quarterly average returns

plot_average.scatter(mort_del, portfolio_q_average)

# Transform daily portfolio_returns returns into quarterly minimum returns

portfolio_q_min = portfolio_returns.resample('Q').min().dropna()

# Create a scatterplot between delinquency and quarterly minimum returns

plot_min.scatter(mort_del, portfolio_q_min)

plt.show()

Least-squares factor model

As we can see, there is a negative correlation between minimum quarterly returns and mortgage delinquency rates from 2005 - 2010. This can be made more precise with an OLS regression factor model.

Dependent variables: average returns, minimum returns, and average volatility.

Independent variable: the mortgage delinquency rate.

In the regression summary, examine the coefficients’ t-statistic for statistical significance, as well as the overall R-squared for goodness of fit.

The statsmodels.api library is available as sm.

1 | # Add a constant to the regression |

分别比较三个因变量的回归系数

results = sm.OLS(port_q_mean, mort_del).fit()results = sm.OLS(port_q_min, mort_del).fit()results = sm.OLS(vol_q_mean, mort_del).fit()

results = sm.OLS(port_q_mean, mort_del).fit() 结果:1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25 OLS Regression Results

==============================================================================

Dep. Variable: y R-squared: 0.021

Model: OLS Adj. R-squared: -0.023

Method: Least Squares F-statistic: 0.4801

Date: Sat, 09 Jan 2021 Prob (F-statistic): 0.496

Time: 05:15:21 Log-Likelihood: 113.89

No. Observations: 24 AIC: -223.8

Df Residuals: 22 BIC: -221.4

Df Model: 1

Covariance Type: nonrobust

=============================================================================================

coef std err t P>|t| [0.025 0.975]

---------------------------------------------------------------------------------------------

const -0.0001 0.001 -0.175 0.862 -0.002 0.002

Mortgage Delinquency Rate 0.0083 0.012 0.693 0.496 -0.016 0.033

==============================================================================

Omnibus: 0.081 Durbin-Watson: 1.604

Prob(Omnibus): 0.960 Jarque-Bera (JB): 0.293

Skew: -0.071 Prob(JB): 0.864

Kurtosis: 2.477 Cond. No. 26.7

==============================================================================

Warnings:

[1] Standard Errors assume that the covariance matrix of the errors is correctly specified.

results = sm.OLS(port_q_min, mort_del).fit()结果:1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25OLS Regression Results

==============================================================================

Dep. Variable: y R-squared: 0.178

Model: OLS Adj. R-squared: 0.141

Method: Least Squares F-statistic: 4.761

Date: Sat, 09 Jan 2021 Prob (F-statistic): 0.0401

Time: 05:17:56 Log-Likelihood: 39.937

No. Observations: 24 AIC: -75.87

Df Residuals: 22 BIC: -73.52

Df Model: 1

Covariance Type: nonrobust

=============================================================================================

coef std err t P>|t| [0.025 0.975]

---------------------------------------------------------------------------------------------

const -0.0279 0.017 -1.611 0.121 -0.064 0.008

Mortgage Delinquency Rate -0.5664 0.260 -2.182 0.040 -1.105 -0.028

==============================================================================

Omnibus: 13.525 Durbin-Watson: 0.513

Prob(Omnibus): 0.001 Jarque-Bera (JB): 12.333

Skew: -1.534 Prob(JB): 0.00210

Kurtosis: 4.710 Cond. No. 26.7

==============================================================================

Warnings:

[1] Standard Errors assume that the covariance matrix of the errors is correctly specified.

results = sm.OLS(vol_q_mean, mort_del).fit()结果:1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25 OLS Regression Results

==============================================================================

Dep. Variable: y R-squared: 0.190

Model: OLS Adj. R-squared: 0.154

Method: Least Squares F-statistic: 5.174

Date: Sat, 09 Jan 2021 Prob (F-statistic): 0.0330

Time: 05:22:24 Log-Likelihood: 60.015

No. Observations: 24 AIC: -116.0

Df Residuals: 22 BIC: -113.7

Df Model: 1

Covariance Type: nonrobust

=============================================================================================

coef std err t P>|t| [0.025 0.975]

---------------------------------------------------------------------------------------------

const 0.0100 0.007 1.339 0.194 -0.006 0.026

Mortgage Delinquency Rate 0.2558 0.112 2.275 0.033 0.023 0.489

==============================================================================

Omnibus: 19.324 Durbin-Watson: 0.517

Prob(Omnibus): 0.000 Jarque-Bera (JB): 23.053

Skew: 1.814 Prob(JB): 9.87e-06

Kurtosis: 6.145 Cond. No. 26.7

==============================================================================

Warnings:

[1] Standard Errors assume that the covariance matrix of the errors is correctly specified.

Morden portforlio throry

The risk-return trade-off

Risk factors: sources of uncertainty affecting return

Intuitively(直觉): greater undcertainty (more risk) compensated by greater return

Cannot guarantee return: need some meaure of expected return

- average (mean) historical return: proxy for expected future return

Investor risk appetite

Investor survey: minimum return required for given level of risk?

Survey response creates (risk. return) risk profile “data point”

Vary risk level => set of (risk, return) points

Investor risk appetite (风险偏好): defines one quantified relationship between risk and return

Choosing portfolio weights

Vary portforlio weights of given portforlio => creates set of (risk, return) pairs

Changing weights = beginning of risk management!

Goal: change weights to maximize expected return, given risk level

- Eyuivalently: minimize risk, given expected return level

Changing weights = adjusting investors’ risk exposure

Morden portforlio throry (MPT)

Efficient portfolio: portfolio with weights generating highest expected return pf given level of risk

The efficient frontier (有效前沿/效率前沿模型)

- Compute many efficient portfolios for different levels of risk

- Efficient frontier(有效边界): locus (轨迹) of (risk, return) pairs created by efficient portfolios

- 有效边界是在收益—风险约束条件下能够以最小的风险取得最大的收益的各种证券的集合

- 处于有效边界上的组合称为有效组合(Efficient Portfolio)

PyPortfolioOpt library: optimized tools for MPTEfficientFrontier class: generates one optimal portfolio at a time

Constrained Line Algorithm (边界算法) class: generate the entire efficient frontier

- Requires covariance matrix of returns)

- Requires proxy for expected future returns: mean historical returns

Invesrment bank portfolio 2005-2010

Expected returns: historical data

Covariance matrix: Covariance Shrinkage improved efficiency of estimate

Constrained Line Algorithm object CLA

Minimum variance portfolio: cla.min_volatility()

Efficient frontier: cla.efficient_frontier()

1 | expected returns = mean_historical_return(prices) |

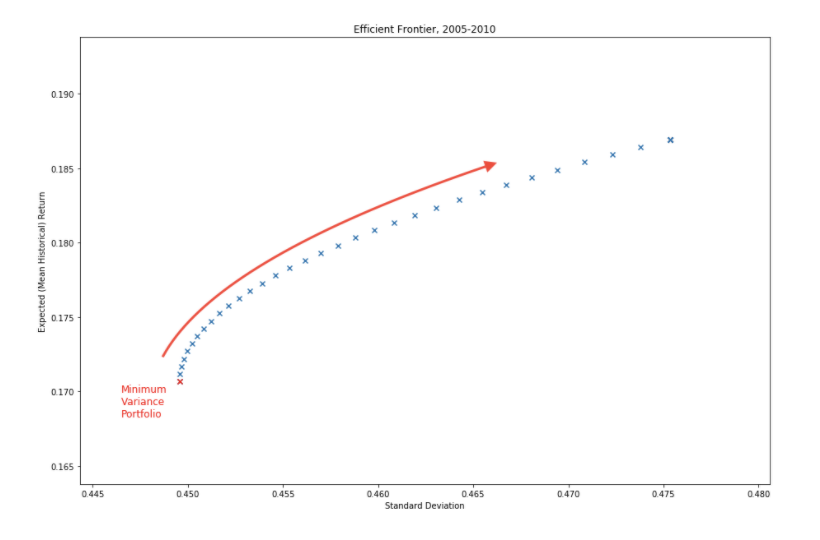

Visualizing the efficient frontier

scatter plot of (vol, ret) pairs

Minimum variance portfolio (最小方差投资组合): smallest volatility of all possible efficient portfolios

Increase risk appetite (增加风险承受能力): move along the frontier

Excercises

Practice with PyPortfolioOpt: returns

Modern Portfolio Theory is the cornerstone of portfolio risk management, because the efficient frontier is a standard method of assessing both investor risk appetite and market risk-return tradeoffs. In this exercise you’ll develop powerful tools to explore a portfolio’s efficient frontier, using the PyPortfolioOpt pypfopt Python library.

To compute the efficient frontier, both expected returns and the covariance matrix of the portfolio are required.

1 | # Load the investment portfolio price data into the price variable. |

Practice with PyPortfolioOpt: covariance

Portfolio optimization relies upon an unbiased and efficient estimate of asset covariance. Although sample covariance is unbiased, it is not efficient—extreme events tend to be overweighted.

One approach to alleviate this is through “covariance shrinkage”, where large errors are reduced (‘shrunk’) to improve efficiency. In this exercise, you’ll use pypfopt.risk_models‘s CovarianceShrinkage object to transform sample covariance into an efficient estimate. The textbook error shrinkage method, .ledoit_wolf(), is a method of this object.

Asset prices are available in your workspace. Note that although the CovarianceShrinkage object takes prices as input, it actually calculates the covariance matrix of asset returns, not prices.

1 | # Import the CovarianceShrinkage object |

结果1

2

3

4

5

6

7

8

9

10

11

12

13Sample Covariance Matrix

Citibank Morgan Stanley Goldman Sachs J.P. Morgan

Citibank 0.536214 0.305045 0.217993 0.269784

Morgan Stanley 0.305045 0.491993 0.258625 0.218310

Goldman Sachs 0.217993 0.258625 0.217686 0.170937

J.P. Morgan 0.269784 0.218310 0.170937 0.264315

Efficient Covariance Matrix

Citibank Morgan Stanley Goldman Sachs J.P. Morgan

Citibank 0.527505 0.288782 0.206371 0.255401

Morgan Stanley 0.288782 0.485642 0.244837 0.206671

Goldman Sachs 0.206371 0.244837 0.225959 0.161823

J.P. Morgan 0.255401 0.206671 0.161823 0.270102

Breaking down the financial crisis

n the video you saw the efficient frontier for the portfolio of investment banks over the entire period 2005 - 2010, which includes time before, during and after the global financial crisis.

Here you’ll break down this period into three sub-periods, or epochs: 2005-2006 (before), 2007-2008 (during) and 2009-2010 (after). For each period you’ll compute the efficient covariance matrix, and compare them to each other.

The portfolio’s prices for 2005 - 2010 are available in your workspace, as is the CovarianceShrinkage object from PyPortfolioOpt.

1 | # Create a dictionary of time periods (or 'epochs') |

结果1

2

3

4

5

6

7

8

9

10

11

12

13

14Efficient Covariance Matrices

{'before': Citibank Morgan Stanley Goldman Sachs J.P. Morgan

Citibank 0.018149 0.013789 0.013183 0.013523

Morgan Stanley 0.013789 0.043021 0.030559 0.016525

Goldman Sachs 0.013183 0.030559 0.044482 0.018237

J.P. Morgan 0.013523 0.016525 0.018237 0.024182, 'during': Citibank Morgan Stanley Goldman Sachs J.P. Morgan

Citibank 0.713035 0.465336 0.323977 0.364848

Morgan Stanley 0.465336 0.994390 0.434874 0.298613

Goldman Sachs 0.323977 0.434874 0.408773 0.224668

J.P. Morgan 0.364848 0.298613 0.224668 0.422516, 'after': Citibank Morgan Stanley Goldman Sachs J.P. Morgan

Citibank 0.841156 0.344939 0.252684 0.356788

Morgan Stanley 0.344939 0.388839 0.231624 0.279727

Goldman Sachs 0.252684 0.231624 0.244539 0.223740

J.P. Morgan 0.356788 0.279727 0.223740 0.382494}

The efficient frontier and the financial crisis

Previously we examined the covariance matrix of the investment bank portfolio before, during and after the financial crisis. Now we will visualize the changes that took place in the efficient frontier, showing how the crisis created a much higher baseline risk for any given return.

Using the PyPortfolioOpt pypfopt library’s Critical Line Algorithm (CLA) object, we can derive and visualize the efficient frontier during the crisis period, and add it to a scatterplot already displaying the efficient frontiers before and after the crisis.

Expected returns returns_during and the efficient covariance matrix ecov_during are available, as is the CLA object from pypfopt. (Remember that DataCamp plots can be expanded to their own window, which can increase readability.)1

2

3

4

5

6

7

8

9

10

11

12

13# Initialize the Crtical Line Algorithm object

efficient_portfolio_during = CLA(returns_during, ecov_during)

# Find the minimum volatility portfolio weights and display them

print(efficient_portfolio_during.min_volatility())

# Compute the efficient frontier

(ret, vol, weights) = efficient_portfolio_during.efficient_frontier()

# Add the frontier to the plot showing the 'before' and 'after' frontiers

plt.scatter(vol, ret, s = 4, c = 'g', marker = '.', label = 'During')

plt.legend()

plt.show()